1. The Spark: Why This Exists

1. The Spark: Why This Exists

Most of us want to save money, but let's face it, adulting is hard. Setting up new apps, navigating complex investment jargon, and remembering to save every month? Meh.

Yet, we use GPay or PhonePe for almost everything. So... what if saving just happened automatically every time we made a payment?

Most of us want to save money, but let's face it, adulting is hard. Setting up new apps, navigating complex investment jargon, and remembering to save every month? Meh.

Yet, we use GPay or PhonePe for almost everything. So... what if saving just happened automatically every time we made a payment?

Assumption-Backed Research Data

Assumption-Backed Research Data

UPI Is Everywhere

UPI Is Everywhere

Over 10 billion UPI transactions happen every month in India. Driven largely by users aged 18–35. (NPCI, 2023)

Over 10 billion UPI transactions happen every month in India. Driven largely by users aged 18–35. (NPCI, 2023)

Gen Z Struggles to Save

Gen Z Struggles to Save

60% of Gen Z in India save less than ₹500/month.

60% of Gen Z in India save less than ₹500/month.

1 in 3 feel overwhelmed by the idea of managing savings manually. (MoneyControl, 2023)

1 in 3 feel overwhelmed by the idea of managing savings manually. (MoneyControl, 2023)

The Demand for Easy, Automated Saving

The Demand for Easy, Automated Saving

Apps like Jar, Fi, and Jupiter have seen 3× growth among 18–30 year olds. (Moloco Case Study)

Apps like Jar, Fi, and Jupiter have seen 3× growth among 18–30 year olds. (Moloco Case Study)

This signifies users crave simplicity in finance tools.

This signifies users crave simplicity in finance tools.

The Financial Literacy Gap

The Financial Literacy Gap

Only 27% of Indians are considered financially literate, and just 16.7% of students grasp basic money management. (OECD, Business Standard).

Only 27% of Indians are considered financially literate, and just 16.7% of students grasp basic money management. (OECD, Business Standard).

The Goal

The Goal

"How might we enable effortless encourage micro-savings for Gen Z and millennials without adding friction to their existing payment behaviour?"

"How might we enable effortless encourage micro-savings for Gen Z and millennials without adding friction to their existing payment behaviour?"

4. Candid Conversations That Sparked the Idea

4. Candid Conversations That Sparked the Idea

4. Candid Conversations That Sparked the Idea

Overwhelmed by Complexity

”I want to save and invest, but honestly the stock market stuff overwhelms me."

— Meenal, 25, UX Designer

Insight: Many users are interested in investing but feel anxious or ill-equipped to navigate complex financial tools.

Friction Blocks Action

"I want to save, but apps like Jar or Groww feel like a big effort. I wish saving was more passive."

— Aditya, 25, Product Manager

Insight: Users value saving but find the onboarding and app-switching experience tedious. Simplicity and integration matter.

Low Visibility = Low Noticing

"Out of sight, out of mind. I don’t notice small spending leaks."

— Aanya, 24, UX Designer

Insight: Micro-spends go unnoticed — but could be powerful saving moments if captured and made visible.

Habitual Use

"I use GPay all the time, even to pay for pani puri. If I saved every time I paid... I’d be rich!"

— Sanika, 22, Student

Insight: UPI platforms like GPay are embedded in daily routines — making them perfect gateways for micro-saving features.

Trust Matters More Than Risk Appetite

"Stock market is intimidating. If GPay could help me save in a way I understand, I’d try it."

— Pratik, 27, Software Engineer

Insight: Users may shy away from volatile investments — but they’re open to trying if it’s via a trusted, familiar app.

Overwhelmed by Complexity

”I want to save and invest, but honestly the stock market stuff overwhelms me."

— Meenal, 25, UX Designer

Insight: Many users are interested in investing but feel anxious or ill-equipped to navigate complex financial tools.

Friction Blocks Action

"I want to save, but apps like Jar or Groww feel like a big effort. I wish saving was more passive."

— Aditya, 25, Product Manager

Insight: Users value saving but find the onboarding and app-switching experience tedious. Simplicity and integration matter.

Low Visibility = Low Noticing

"Out of sight, out of mind. I don’t notice small spending leaks."

— Aanya, 24, UX Designer

Insight: Micro-spends go unnoticed — but could be powerful saving moments if captured and made visible.

Habitual Use

"I use GPay all the time, even to pay for pani puri. If I saved every time I paid... I’d be rich!"

— Sanika, 22, Student

Insight: UPI platforms like GPay are embedded in daily routines — making them perfect gateways for micro-saving features.

Trust Matters More Than Risk Appetite

"Stock market is intimidating. If GPay could help me save in a way I understand, I’d try it."

— Pratik, 27, Software Engineer

Insight: Users may shy away from volatile investments — but they’re open to trying if it’s via a trusted, familiar app.

Ideation Journey

Ideation Journey

Exploring How Smart Saving Could Work on GPay, To define the right saving behaviour, I started with key How Might We questions:

Exploring How Smart Saving Could Work on GPay, To define the right saving behaviour, I started with key How Might We questions:

How can I help people save money without even trying, or downloading yet another app?

What if saving money was as easy as checking a box after your next GPay transaction?

Can I make saving so simple, you forget you’re even doing it?

How do I turn everyday GPay payments into guilt-free little savings wins?

How can I help people save money without even trying, or downloading yet another app?

What if saving money was as easy as checking a box after your next GPay transaction?

Can I make saving so simple, you forget you’re even doing it?

How do I turn everyday GPay payments into guilt-free little savings wins?

Ideas Explored 💡

Ideas Explored 💡

Daily/Weekly Auto-Saving Rules

User selects a fixed amount (₹50/week or ₹10/day).

❌ Felt like a chore. Lacks flexibility. Easy to forget or disable.

Save Your Cash back

Redirect cash back into a wallet or micro-investment.

✅ Effortless, ❌ but cash backs are small + unpredictable = low motivation.

Spare Change Round-ups

Spend ₹97, save the leftover ₹3 into savings.

✅ Good concept, ❌ but depends on random math, user will not have fixed clarity

Goal-Based Savings Tracker

Users set goals like “New phone ₹10,000 by Oct,” and save manually.

✅ Strong motivation, ❌ needs efforts to setup, and doesn’t work passively.

Gamified Savings Challenges

Save ₹50 every day for 30 days = unlock rewards.

✅ Fun for some, ❌ but can feel forced and gimmick. Doesn’t suit all personalities.

Final Pick:

Smart Save with % Cut Per Transaction (2%, 5%, 10%)

How it works:

Users sign up once and choose a saving percentage (2%, 5%, or 10%).

From then on, every time they pay via GPay, that % is automatically saved.

Want to skip it? Just uncheck the Smart Save box before you enter your UPI PIN.

✅ Why this works:

Effortless yet customizable: One-time setup, works in the background.

Builds into as a habit.

Gives control, not pressure, Toggle it off any time before payment.

Feels light and non-intrusive. Seemless integration, low-commitment, high return.

Builds trust and delight. Users see small wins growing over time.

This solution checked all the boxes: low effort, high familiarity, emotionally rewarding, and frictionless.

Daily/Weekly Auto-Saving Rules

User selects a fixed amount (₹50/week or ₹10/day).

❌ Felt like a chore. Lacks flexibility. Easy to forget or disable.

Save Your Cash back

Redirect cash back into a wallet or micro-investment.

✅ Effortless, ❌ but cash backs are small + unpredictable = low motivation.

Spare Change Round-ups

Spend ₹97, save the leftover ₹3 into savings.

✅ Good concept, ❌ but depends on random math, user will not have fixed clarity

Goal-Based Savings Tracker

Users set goals like “New phone ₹10,000 by Oct,” and save manually.

✅ Strong motivation, ❌ needs efforts to setup, and doesn’t work passively.

Gamified Savings Challenges

Save ₹50 every day for 30 days = unlock rewards.

✅ Fun for some, ❌ but can feel forced and gimmick. Doesn’t suit all personalities.

Final Pick:

Smart Save with % Cut Per Transaction (2%, 5%, 10%)

How it works:

Users sign up once and choose a saving percentage (2%, 5%, or 10%).

From then on, every time they pay via GPay, that % is automatically saved.

Want to skip it? Just uncheck the Smart Save box before you enter your UPI PIN.

✅ Why this works:

Effortless yet customizable: One-time setup, works in the background.

Builds into as a habit.

Gives control, not pressure, Toggle it off any time before payment.

Feels light and non-intrusive. Seemless integration, low-commitment, high return.

Builds trust and delight. Users see small wins growing over time.

This solution checked all the boxes: low effort, high familiarity, emotionally rewarding, and frictionless.

What’s in it for GPay?

What’s in it for GPay?

Increased Engagement Time

Increased Engagement Time

Micro-savings add emotional value to every transaction. Users revisit the app not just to pay, but to track, celebrate, and grow their savings.

Micro-savings add emotional value to every transaction. Users revisit the app not just to pay, but to track, celebrate, and grow their savings.

Strengthens Trust & Stickiness

Strengthens Trust & Stickiness

By helping users build healthy saving habits, GPay becomes more than a utility. It becomes a financial ally users won’t switch from.

By helping users build healthy saving habits, GPay becomes more than a utility. It becomes a financial ally users won’t switch from.

Boosts Monthly Active Users (MAUs)

Boosts Monthly Active Users (MAUs)

With the "Smart Save" feature nudging repeat visits, you drive habit loops that increase app retention and daily usage.

With the "Smart Save" feature nudging repeat visits, you drive habit loops that increase app retention and daily usage.

Differentiation from Competitors

Differentiation from Competitors

While other UPI apps focus only on payments, GPay integrates micro-finance with simplicity. A unique value prop in a saturated market.

While other UPI apps focus only on payments, GPay integrates micro-finance with simplicity. A unique value prop in a saturated market.

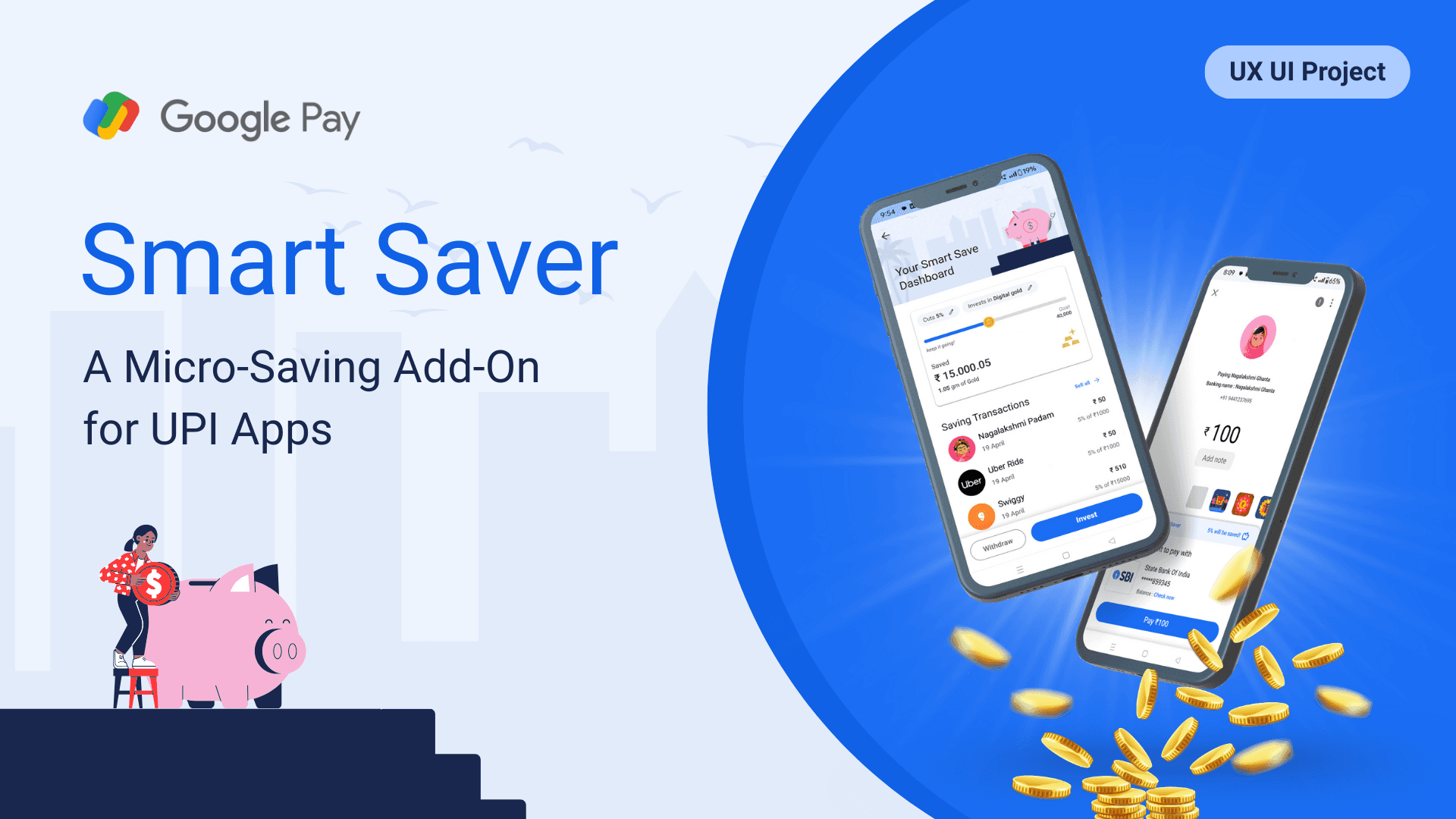

Solution Overview

Solution Overview

Onboarding: Set your saving % (2%, 5%, or 10%) and preferred investment type (Gold, Equity, Wallet).

Payment Flow : Each time you make a GPay transaction, the selected % is automatically saved.

You can toggle it OFF during payment, right before UPI PIN entry.

Smart Save Dashboard : Track your total savings, investment performance, and progress toward optional goals.

Withdraw or Invest More : Withdraw instantly or boost your savings manually anytime.

Onboarding: Set your saving % (2%, 5%, or 10%) and preferred investment type (Gold, Equity, Wallet).

Payment Flow : Each time you make a GPay transaction, the selected % is automatically saved.

You can toggle it OFF during payment, right before UPI PIN entry.

Smart Save Dashboard : Track your total savings, investment performance, and progress toward optional goals.

Withdraw or Invest More : Withdraw instantly or boost your savings manually anytime.

Where it fits in? - Information Architecture

Where it fits in? - Information Architecture

Onboarding : Set your saving % (2%, 5%, or 10%) and preferred investment type (Gold, Equity, Wallet).

Payment Flow : Each time you make a GPay transaction, the selected % is automatically saved.

You can toggle it OFF during payment, right before UPI PIN entry.

Smart Save Dashboard : Track your total savings, investment performance, and progress toward optional goals.

Withdraw or Invest More : Withdraw instantly or boost your savings manually anytime.

Onboarding : Set your saving % (2%, 5%, or 10%) and preferred investment type (Gold, Equity, Wallet).

Payment Flow : Each time you make a GPay transaction, the selected % is automatically saved.

You can toggle it OFF during payment, right before UPI PIN entry.

Smart Save Dashboard : Track your total savings, investment performance, and progress toward optional goals.

Withdraw or Invest More : Withdraw instantly or boost your savings manually anytime.

A brief information architecture diagram

. What goes where ? ( Wire framing )

. What goes where ? ( Wire framing )

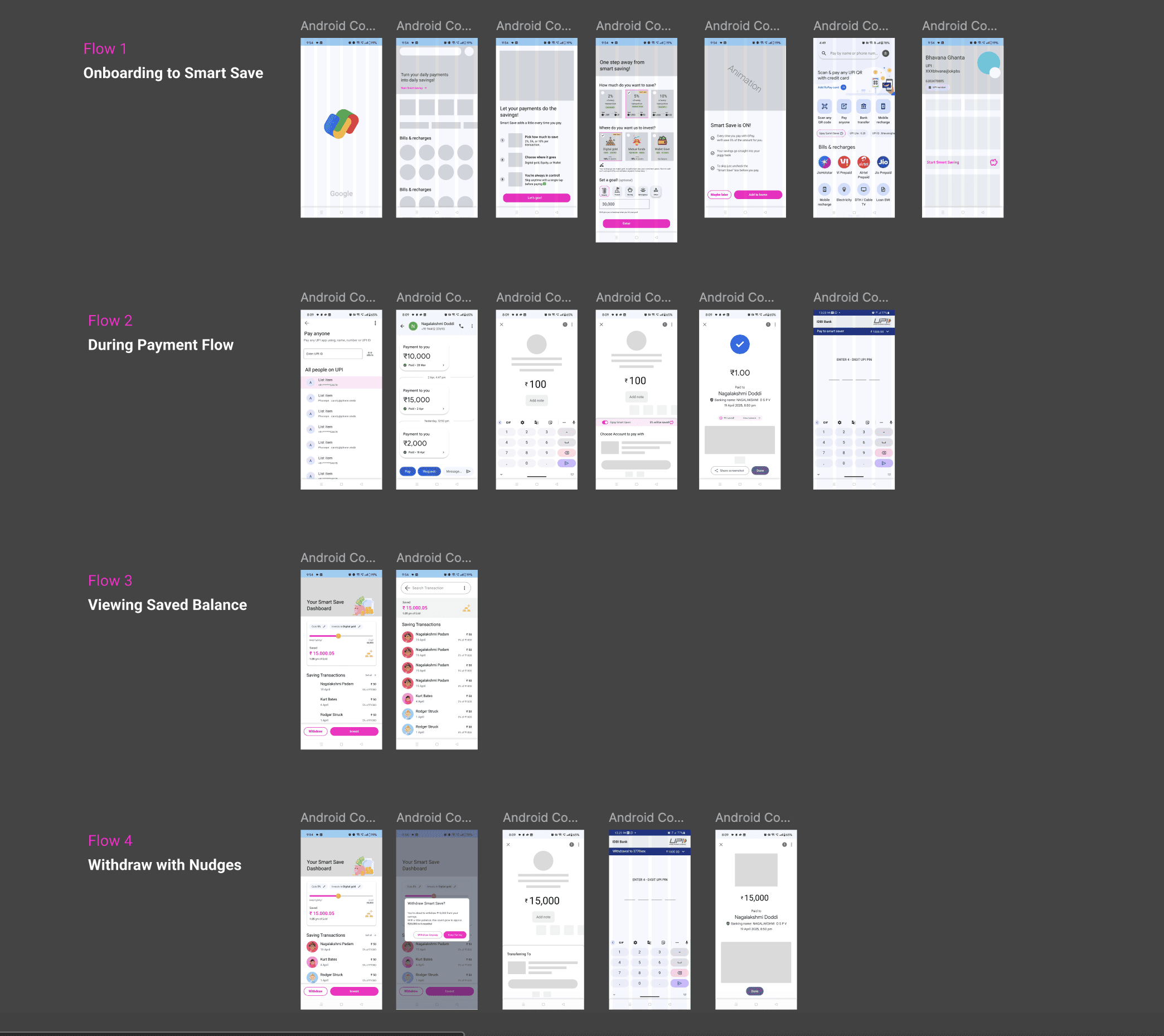

I created low-fidelity wireframes to quickly visualize the structure and key flows of the feature.

This helped me map out the user journey, placement, and interactions before moving to high-fidelity designs.

I created low-fidelity wireframes to quickly visualize the structure and key flows of the feature.

This helped me map out the user journey, placement, and interactions before moving to high-fidelity designs.

High level wire framing, colour the main highlights in pink.

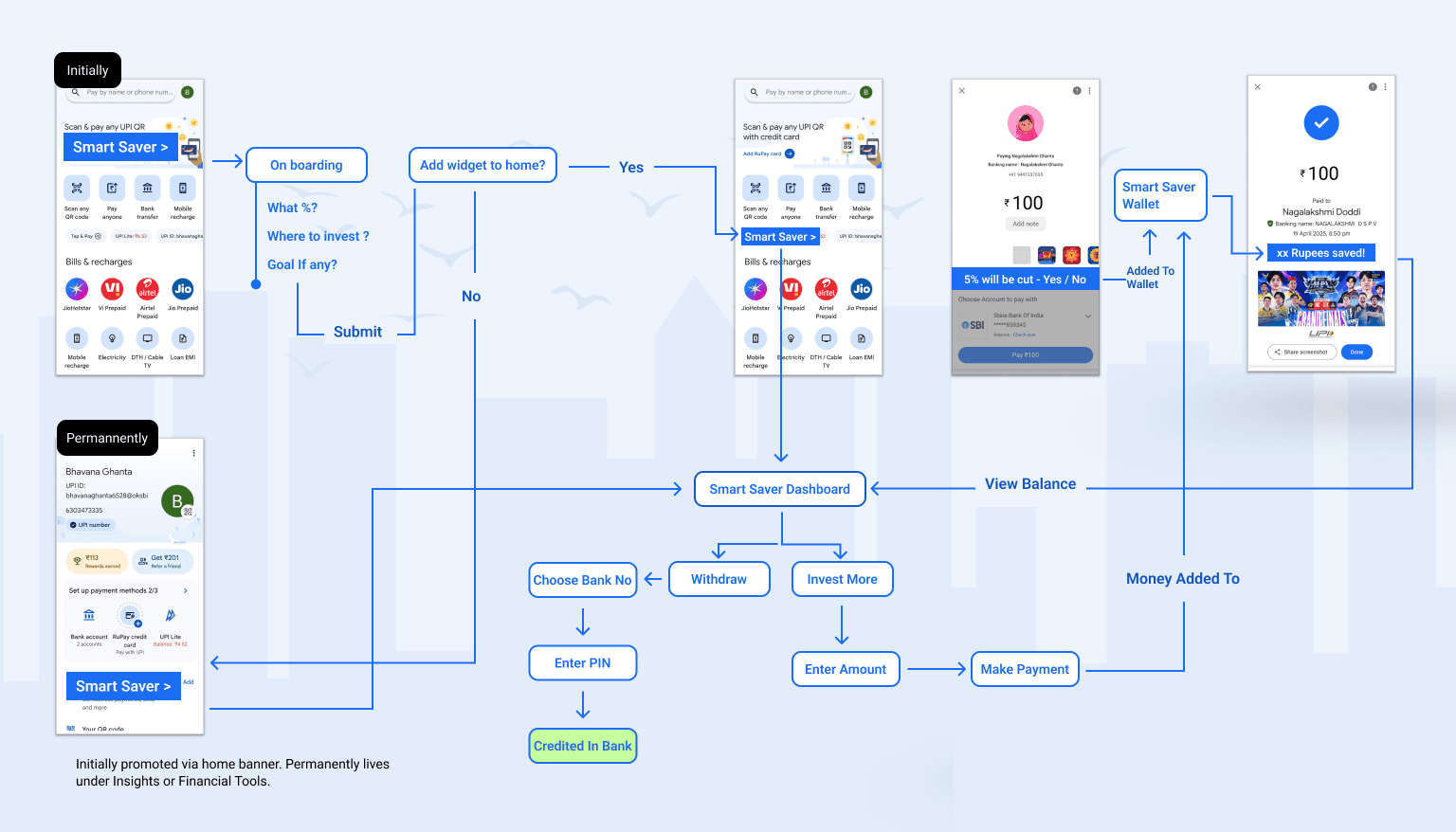

Flow I : Onboarding to Smart Save!

Flow I : Onboarding to Smart Save!

Flow

Prompt users with “Start Smart Saving?”

Let them choose a percentage (2%, 5%, 10%)

Set and forget—works silently in the background

Pros

Personalisation increases ownership & stickiness

Gives control and flexibility (not one-size-fits-all)

Seamless after the setup, low effort

Features Notes

default “Recommended” setting (e.g., 5%) for faster onboarding

Visual examples like: “Pay ₹500, we’ll save ₹25.”

Assumptions

Users trust Google Pay enough to allow auto-deductions

Users want to customize how much they save

Too much effort in onboarding might lead to drop-offs

Flow

Prompt users with “Start Smart Saving?”

Let them choose a percentage (2%, 5%, 10%)

Set and forget—works silently in the background

Pros

Personalisation increases ownership & stickiness

Gives control and flexibility (not one-size-fits-all)

Seamless after the setup, low effort

Features Notes

default “Recommended” setting (e.g., 5%) for faster onboarding

Visual examples like: “Pay ₹500, we’ll save ₹25.”

Assumptions

Users trust Google Pay enough to allow auto-deductions

Users want to customize how much they save

Too much effort in onboarding might lead to drop-offs

Flow II : During Payment Flow

Flow II : During Payment Flow

Flow

Every time a user pays, 5% gets saved

Users can switch this off from the payment screen (toggle)

Pros

Subtle nudge at high-intent moment

Builds habit through repetition

Offers control without going into settings

Features Notes

fun, tiny animation or icon (like a piggy bank filling)

Snack-bar messages - “₹25 saved! Tap to see more.”

Assumptions

Users will notice and understand the toggle

5% feels small enough to not hurt spending

Users want control at the moment of payment

Flow

Every time a user pays, 5% gets saved

Users can switch this off from the payment screen (toggle)

Pros

Subtle nudge at high-intent moment

Builds habit through repetition

Offers control without going into settings

Features Notes

fun, tiny animation or icon (like a piggy bank filling)

Snack-bar messages - “₹25 saved! Tap to see more.”

Assumptions

Users will notice and understand the toggle

5% feels small enough to not hurt spending

Users want control at the moment of payment

Flow III : Viewing Dashboard

Flow III : Viewing Dashboard

Flow

The user can view the payment till data, amount invested and the transactions

This dashboard can be navigated from home screen or under the profile icon page.

Pros

Emotional reinforcement builds habit

Encourages revisiting the feature

Helps users internalise “I am a saver!”

Features Notes

Use progress rings or “jar filling up” animations

User can view the goals they have set.

Badge levels fro user like “Tiny Saver…

Assumptions

Visual celebration improves habit stickiness

Users love gamification and progress

Flow

The user can view the payment till data, amount invested and the transactions

This dashboard can be navigated from home screen or under the profile icon page.

Pros

Emotional reinforcement builds habit

Encourages revisiting the feature

Helps users internalise “I am a saver!”

Features Notes

Use progress rings or “jar filling up” animations

User can view the goals they have set.

Badge levels fro user like “Tiny Saver…

Assumptions

Visual celebration improves habit stickiness

Users love gamification and progress

Flow IV : Withdraw And Invest With Nudges

Flow IV : Withdraw And Invest With Nudges

Flow

Users can withdraw and Invest at any time.

The app should encourage them to stay longer.

Pros

Flexibility = trust

Nudges can delay unnecessary withdrawals

Keeps savings feel like your money, not “locked away”

Features Notes

popup msgs like: “Withdraw ₹500 now or leave it until xxx to reach ₹XXX?”

Offer “Withdraw partially” as primary actions.

Assumptions

People withdraw impulsively unless nudged

Users may not know the long-term benefit of keeping money saved

Flow

Users can withdraw and Invest at any time.

The app should encourage them to stay longer.

Pros

Flexibility = trust

Nudges can delay unnecessary withdrawals

Keeps savings feel like your money, not “locked away”

Features Notes

popup msgs like: “Withdraw ₹500 now or leave it until xxx to reach ₹XXX?”

Offer “Withdraw partially” as primary actions.

Assumptions

People withdraw impulsively unless nudged

Users may not know the long-term benefit of keeping money saved

Did You Notice These Little Visual Joys?

Did You Notice These Little Visual Joys?

Smart Save isn't just functional, it should be delightful.

To make the experience feel more approachable and intuitive, I crafted custom illustrations like the cheerful Piggy Bank, expressive coin animations, and playful goal-setting icons.

These visuals not only guide users through the journey, but also celebrate every small win, turning everyday payments into something worth smiling about.

Because saving money should feel just as rewarding as spending !

Smart Save isn't just functional, it should be delightful.

To make the experience feel more approachable and intuitive, I crafted custom illustrations like the cheerful Piggy Bank, expressive coin animations, and playful goal-setting icons.

These visuals not only guide users through the journey, but also celebrate every small win, turning everyday payments into something worth smiling about.

Because saving money should feel just as rewarding as spending !

That’s a wrap!

That’s a wrap!

Thanks for scrolling through, would love to hear your thoughts, feedback, or even just a Hi !

Thanks for scrolling through, would love to hear your thoughts, feedback, or even just a Hi !